Article

9 Feb 2026

Case Study: AUDJPY Breakout

This case study examines a breakout-based MT4 Expert Advisor tested on AUDJPY using a $10,000 baseline account. The strategy is designed to trade volatility expansions during key session opens, with strict risk constraints and defined drawdown limits.

Strategy Overview

The EA is built around session breakout logic. It waits for price to break beyond a defined lookback range during major liquidity transitions, specifically:

Asia session open

London session open

Fixed lookback period defining breakout levels

Risk-defined position sizing per trade

The objective is to capture directional momentum immediately following volatility expansion rather than mean reversion.

Backtest Configuration

Instrument: AUDJPY

Timeframe: M5

Data range: 1 January 2021 – 16 May 2025

Account size: $10,000

Risk per trade: ~$1,000 (10%)

Execution model: breakout continuation

Session triggers: Asia open and London open (UTC+2 broker time)

Hypothesis

AUDJPY exhibits a systematic tendency to make a directional breakout within the first 90 minutes of the Sydney session open, driven by the confluence of returning Asian liquidity, Australian institutional order flow, and the AUD/JPY cross's sensitivity to risk sentiment shifts that accumulate during the overnight New York close. The strategy exploits this recurring volatility expansion window by entering on breakout confirmation and exiting at a defined target or stop.

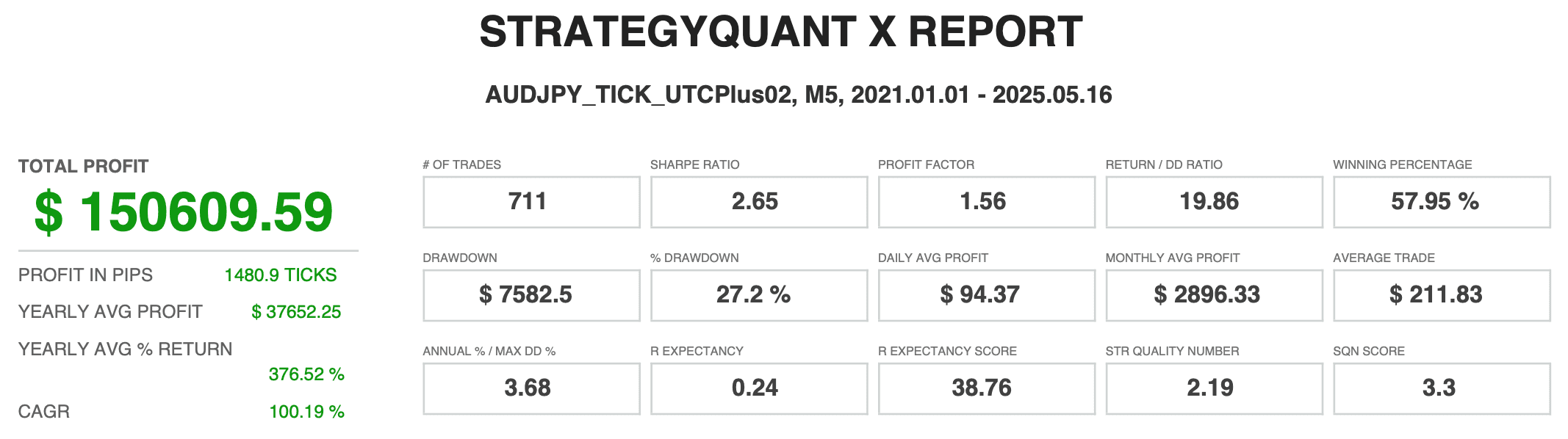

Performance Summary

The backtest generated strong risk-adjusted returns over the testing period.

Total trades: 711

Win rate: 57.95%

Gross profit: $418,659

Gross loss: $268,049

Net profit: $150,609

Sharpe ratio: 2.65

Profit factor: 1.56

Max drawdown: $7,582

Return / drawdown ratio: 19.86

Average trade: $211.83

CAGR: ~100%

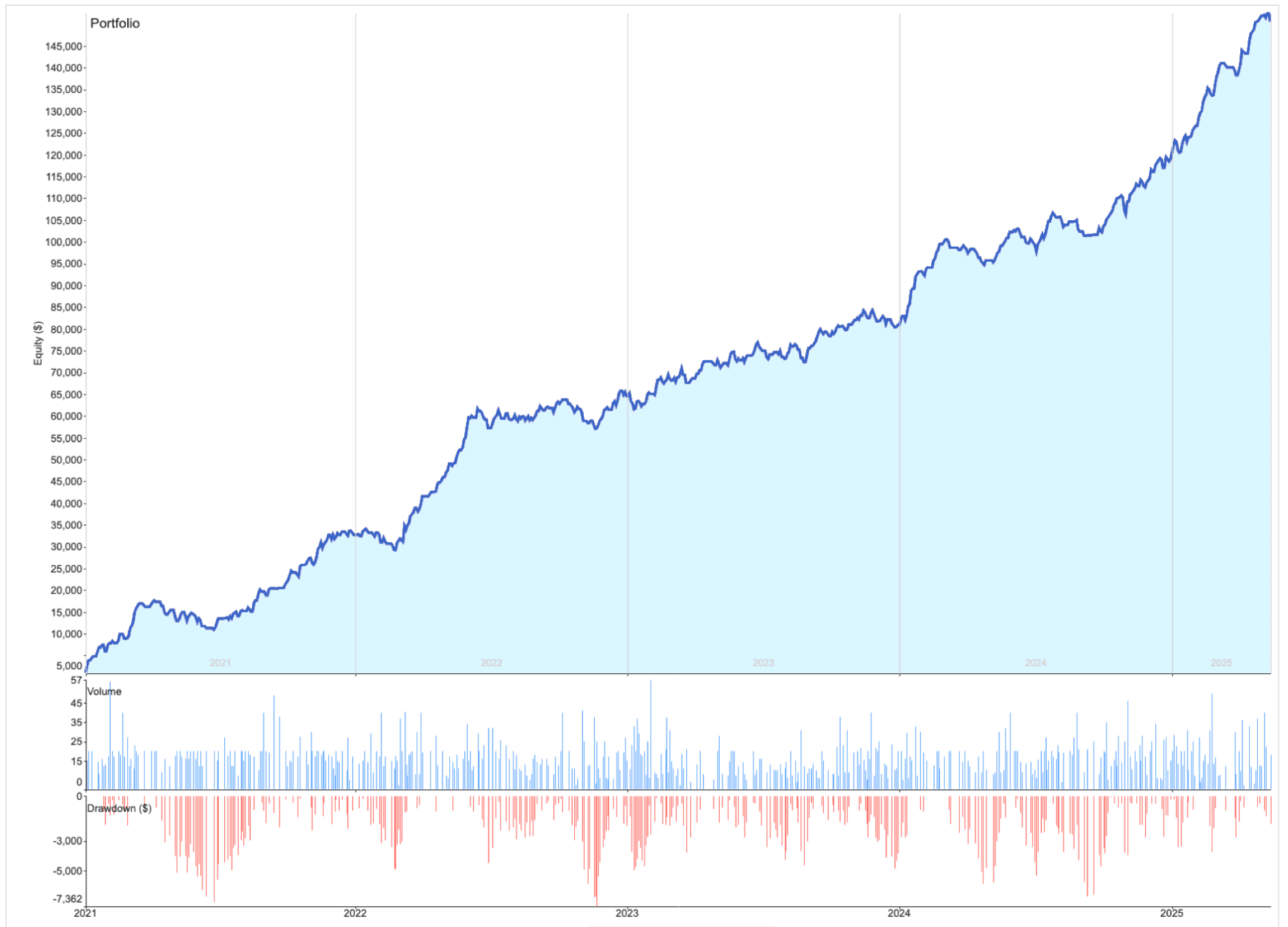

The equity curve shows consistent upward progression with manageable stagnation periods (~140 days).

Risk Structure

The system was intentionally configured to risk approximately $1,000 per trade on a $10,000 account, equivalent to 10% exposure. This creates an intentionally aggressive testing scenario designed to stress-test drawdown behaviour.

Under this configuration:

Maximum drawdown remained below $8,000

Drawdown stayed within ~27% peak-to-valley range

Winning percentage remained close to 58%

This suggests the underlying logic is resilient even under elevated risk conditions.

Prop Firm Scenario Example

If applied to a $100,000 prop firm account, the same logic can be scaled conservatively:

Maintain absolute risk at $1,000 per trade

This becomes 1% risk instead of 10%

Effective drawdown ceiling remains ~$10,000

Keeps trading within a typical 10% max drawdown rule

This demonstrates that the strategy architecture can be adapted to stricter risk environments without altering core logic.

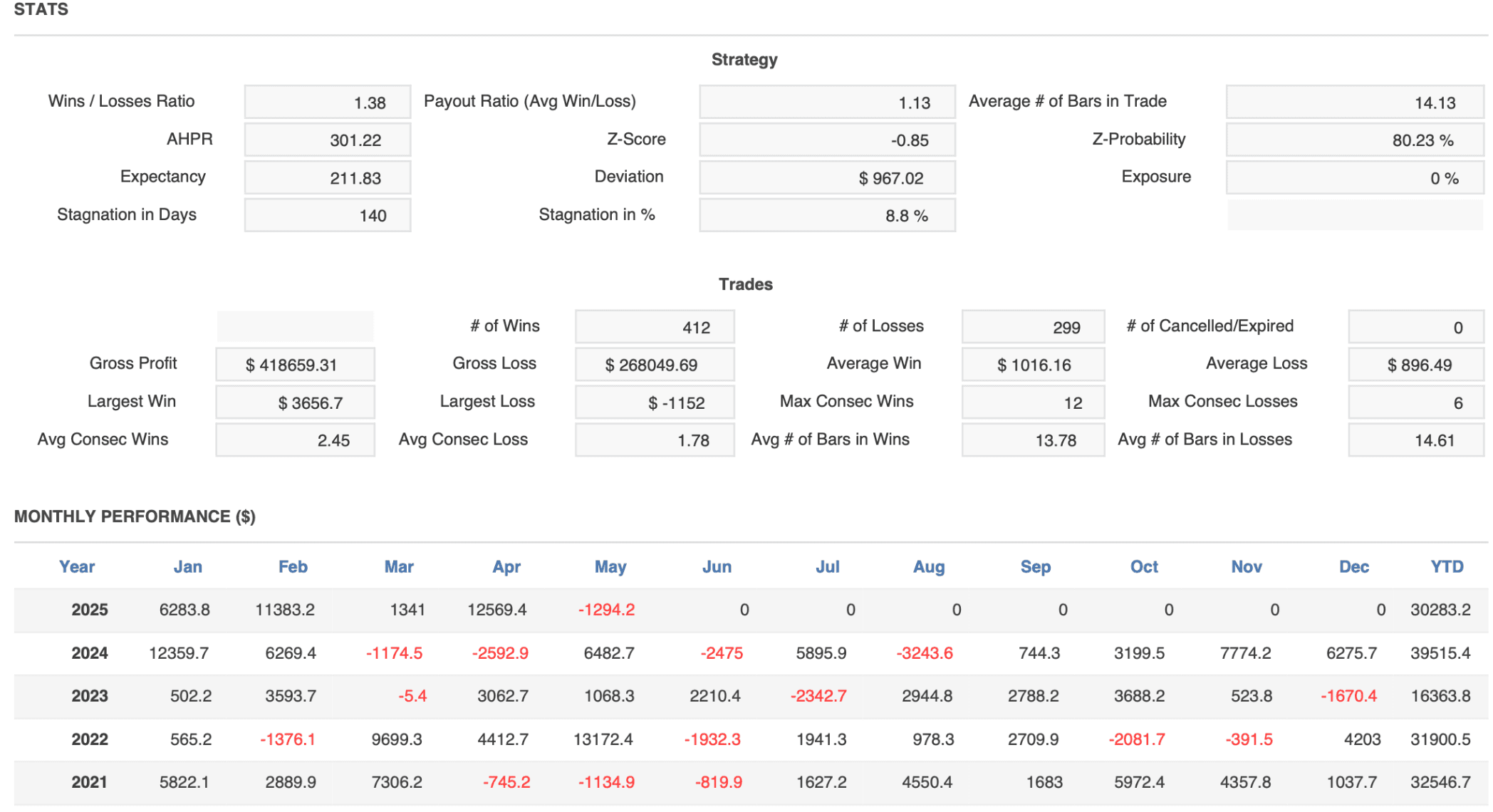

Trade Behaviour Characteristics

The strategy exhibits:

Strong but realistic win rate (~58%)

Slightly larger average wins than losses

Limited consecutive losses (max observed: 6)

Short trade durations (average ~14 bars)

These properties are consistent with breakout continuation systems that rely on momentum bursts rather than long trend holding.

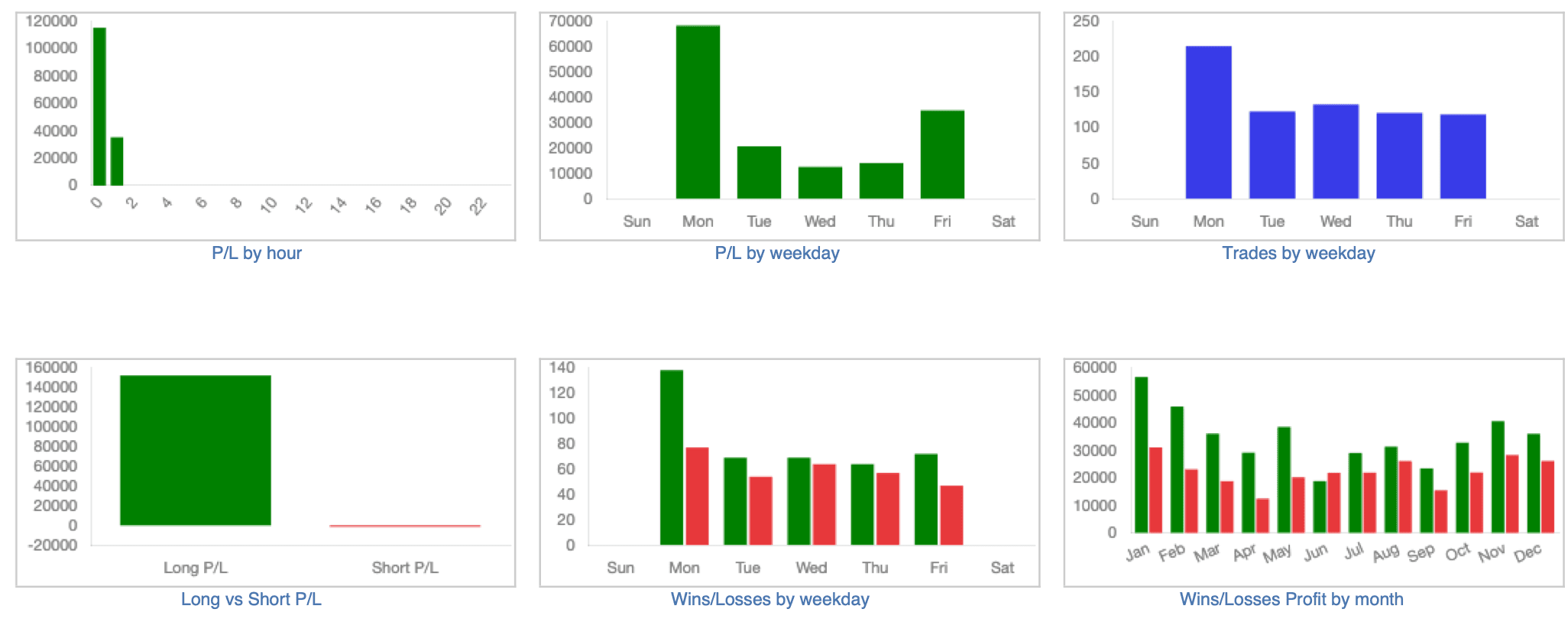

Session-Based Edge

Preliminary breakdowns indicate stronger performance during high-volatility session transitions. In particular:

London open breakouts produced consistent directional follow-through

Asia session volatility expansion also contributed materially

Monday behaviour shows potential for optimisation

Further refinement could include:

Restricting trading to specific weekdays

Adjusting lookback windows per session

Volatility filters prior to entry

These are optimisation paths rather than structural requirements.

Strategy Logic Summary

Identify consolidation range using defined lookback

Wait for breakout during Asia or London session open

Enter in breakout direction

Apply fixed risk-based position sizing

Exit via predefined TP/SL logic

The design emphasises simplicity, repeatability, and controlled exposure.

Key Takeaways

The EA demonstrates stable performance across multiple years

Drawdown remains contained relative to return

Risk can be scaled linearly across account sizes

Session-based volatility is the primary driver

Additional optimisation opportunities exist

Notes on Interpretation

This is a historical backtest using broker-time UTC+2 data. Results may vary depending on:

Broker execution

Spread differences

Slippage

Liquidity conditions

The purpose of this case study is to illustrate behaviour and risk characteristics rather than guarantee performance.